Get started

How to use this document

Look out for the flashing panels - As you turn each page, you will see flashing panels briefly appear. These panels indicate links to more information or email addresses where you can request more info. Searching for something? Click on the three lines on the bottom left hand side of the page, select search and enter your keyword. Futher questions or comments? Please email HRDirect@quilter.com

Suitable for retail clients.

Investing in uncertain times

Contents

Invest early

4

Beware of inflation

5

Diversify your investments

6

Invest for the long term (growth)

7

Invest for the long term (bull and bear)

8

Invest for the long term (market drawdowns)

9

Helping you invest in uncertain times

3

Your next step

11

Important information

12

Stay invested

10

The current economic conditions present financial challenges. However, history shows that getting financial advice and investing with a long-term outlook is key to achieving your financial goals. Here is your three-step plan.

Speak to a financial adviser and get some expert advice. They can help to put your mind at ease about whether you are doing the right thing. They can also help to take the emotion out of investing and provide an objective view. It may just be the best investment you ever make.

Making your environment comfortable

Find out more about this here

Over the following pages we have put together some helpful charts and diagrams that demonstrate the benefits and advantages of a long-term, diversified approach to investing. Click here to download this guide.

• Use a cushion or pillow to sit on or support your back if you are uncomfortable. • Avoid sitting in bright sunlight which can cause glare on the screen. • Stretch and change position often; getting up and walking around can help. • Moving your arms and shoulders can relieve the tension that is caused by sitting in the same position for prolonged periods of time. • Look away from your screen frequently; try looking into the distance and remember to blink often. • Don’t wait until you are uncomfortable before you take a break. • Short, frequent breaks are better than longer, infrequent ones to prevent discomfort.

1. Get financial advice

Your money needs to be in the right place to recover in value and make a profit if markets go up, so it is important not to sell an investment as a knee-jerk reaction if its value goes down temporarily. it is vital to make a long-term investment plan, stick to it, and do not try to time the market.

2. Have a long-term financial plan

It is best to invest in a range of different places where your money has a chance to grow. You should always hold some funds in cash in case of an emergency, but other investments offer better growth potential. By spreading money across different investment types, it is possible to avoid exposing your portfolio to undue risk.

3. Make sure your investments are diversified

Back to contents

The value of investments can fall as well as rise. You might get back less than you invested.

Compound interest – earning interest on your interest – can have an incredible effect on your investments.

The chart below shows the benefits of investing as early as possible. Over the past 30 years, an investor could have accumulated £56,194 more than someone who started investing five years later, even though they both invested £10,000. If the later investor wanted to accumulate the same amount they would have needed to make an initial investment of £18,011.

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance. Source: Quilter and Morningstar as at 31 December 2025. Total return, percentage growth over period 1 January 1996 to 31 December 2025 of the MSCI All Country World Index. Based on an initial investment of £10,000.

Key takaways

Invest as early and as soon as you can. Grow your investments quicker by earning interest on your interest. Avoid withdrawing money to boost the effects of compound interest.

Return (£)

It is tempting to see cash as a safe haven against market volatility, but inflation can be very damaging to your investments.

The chart below demonstrates how inflation of just three percent can reduce the value of cash by almost half over a twenty year period. Inflation can be incredibly corrosive to any savings held in cash.

Inflation can be devastating to your savings over the long term. Holding your investments in cash does not provide any protection against inflation. Cash should only be held for an emergency or for short- to medium-term income purposes.

£6,730

£5,537

£3,769

Volatility is the extent and speed of change in the value of a financial security such as a bond or equity. The greater the movements in the price of a security, and the shorter the timeframe of such changes, the higher its volatility. The higher the volatility of an asset, the more unpredictable and extreme its price movements.

Inflation is the rate of increase in the price of goods and services. For most countries, it’s based on a basket of items that are assumed to represent the cost of living. Inflation increases the cost of goods and services but decreases the real value of cash savings.

Source: Quilter and Morningstar as at 31 December 2025. This information provided is for illustrative purposes only and does not represent the past performance of any particular investment. Based on an initial investment of £10,000.

By spreading your money across different types of assets, it is possible to avoid exposing your investments to undue risk.

The jumble of colours below – with each colour representing a different type of asset – shows how varied the performance of equities (company shares), bonds, and property has been over the past 10 years. There is no guarantee that the investment that is top in one year will perform well in the next.

Best

Worst

Return (%)

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance. Source: Quilter and Morningstar as at 31 December 2025. Discrete annual return, percentage growth over period 1 January 2016 to 31 December 2025. Equities are represented by the the appropriate MSCI index, commodities by the Bloomberg Commodity Index, global bonds by the Bloomberg Global Aggregate Index, UK gilts by the ICE BofA UK Gilt Index, and UK property by the IA UK Direct Property sector average.

Spread your money across a range of different investments to reduce risk. Do not assume that the past performance of an investment will reflect its future performance. Investing in a range of assets is likely to be more successful than trying to pick just one or two.

Equities are company shares. In most instances, except for private equity, they describe shares in listed companies that are traded on recognised stock markets. Being a shareholder confers a right to a share in a company’s profits that are distributed as dividends.

Bonds are fixed-income investments that represent a loan made by an investor to a borrower such as a government, company, or large institution. In principle, bond investors are lending money (the principal) to the bond issuer in return for a fixed or variable rate of interest (coupon) during the term of the bond. When the term ends (maturity), the issuer repays the principal to the investor.

Property, also known as real estate, is the term for investments in housing or other real-estate assets, such as retail sites and shops, office buildings, warehousing, logistics sites, and industrial premises.

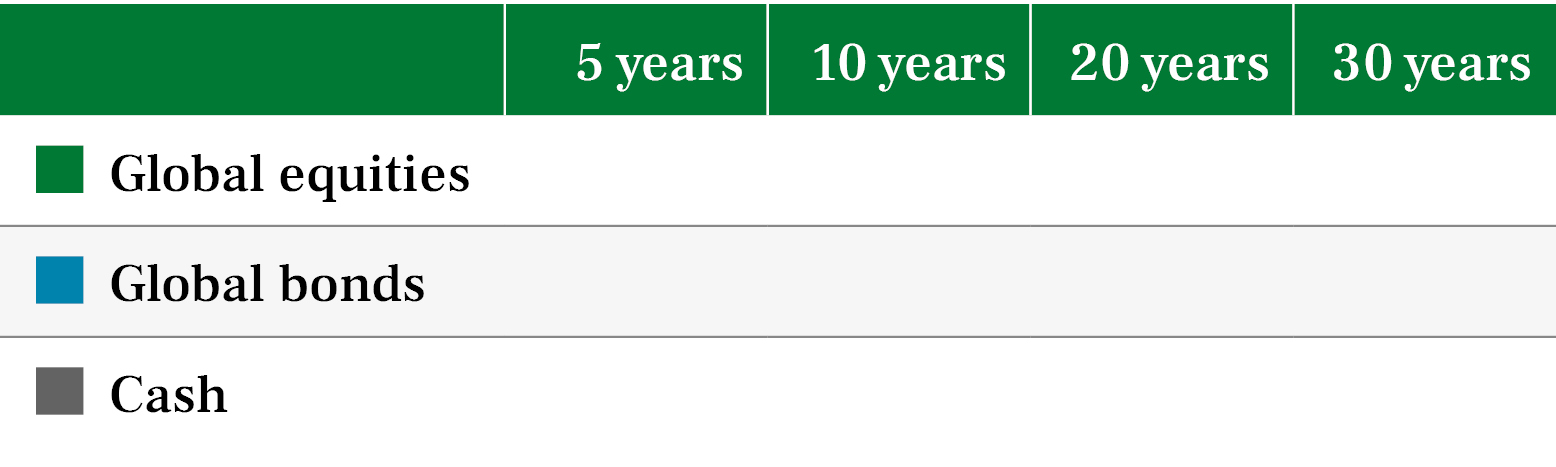

Investing with a long-term outlook is the best way for you to reduce the impact of stock market fluctuations and to grow your investments over time.

The chart below shows that over the long term, there is an upward trend of returns from equities and bonds, despite the short-term volatility caused by major events. In fact, an investment into global equities could have grown to be worth more than 12 times its original value over the past 30 years.

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance. Source: Quilter and Morningstar as at 26 March 2026. Total return, percentage growth over period 1 January 1996 to 26 March 2026. Based on an initial investment of £10,000. Global equities are represented by the MSCI All Country World Index, global bonds by the Bloomberg Global Aggregate Index, and cash by the Bank of England Base Rate.

Do not let short-term blips distract you from your long-term plan. People who stay invested are more likely to see their investments recover. Investing over the longer term (five years or more) is more likely to be successful.

Cumulative returns

5 years

10 years

20 years

30 years

78%

3%

7%

Global equities

Global bonds

Cash

Click here to see the returns over different time periods

77%

249%

582%

1,163%

-1%

17%

87%

310%

19%

43%

139%

Bull and bear markets are a feature of investing, but bull markets have typically lasted longer and returned more.

The chart below shows that over the past 30 years global equity bull markets (when an index rises by 20% or more from a recent low) have historically gone on for longer and delivered higher returns than bear markets (when an index falls by 20% or more from a recent high).

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance. Source: Quilter and Morningstar as at 31 December 2025. Total return, percentage growth over period 1 January 1996 to 31 December 2025. Global equities are represented by the MSCI All Country World Index.

Bull and bear markets are a normal feature of investing. Bull markets have historically gone on for longer and delivered higher returns. A long-term approach to investing is the best strategy to achieve financial growth.

Source: Quilter Investors and Morningstar as at 31 December 2024. Total return, percentage growth over period 31 December 1994 to 31 December 2024.

75%

213%

599%

1,156%

85%

334%

14%

142%

Markets often fall, and can do so sharply, but this does not mean they will return a loss for the entire year.

The chart below shows that while markets often have periods in every year where they decline, the overall picture is far better. Over the past 30 years, an investment into global equities would have experienced intra-year declines every year, but would have only been down at the end of the year on seven occasions.

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance. Source: Quilter and Morningstar as at 31 December 2025. Discrete annual return, percentage growth and maximum annual drawdown over period 1 January 1996 to 31 December 2025 of the MSCI All Country World Index.

Investment markets often see blips throughout the year. Overall, global equities end the year up far more than they end it down. Staying invested is the best strategy for achieving long-term financial growth.

Source: Quilter and Morningstar as at 30 June 2025. Total return, percentage growth over time periods shown to 30 June 2025.

During periods of volatility it can be tempting to exit the market, but missing just a few of the best days can have a big impact on your overall return.

The chart below shows that someone who stayed invested in global equities over the past 30 years, could have received a potential return more than four times greater than someone who missed the best 25 days.

Time in the market is usually more successful than trying to time the market. Keeping your money invested means you can benefit from any upsides or bounces. Missing just a few good days can significantly reduce how much your investment grows.

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance. Source: Quilter and Morningstar as at 31 December 2025. Total return in pounds sterling over period 1 January 1996 to 31 December 2025 of the MSCI All Country World Index.

We are dedicated to making sure your investment journey with us is as smooth as possible. Please visit our website at quilter.com for all the latest news, views, and portfolio information.

Before making any decisions, we recommend you speak to your financial adviser and get some expert advice. Your financial adviser is responsible for understanding your specific investment objectives and appetite for risk. They will work closely with you to determine what is right for you.

If you are a financial adviser and want to find out more about our investment solutions, please speak to one of our investment directors on 0207 167 3700, email us at enquiries@quilter.com, or visit our website at quilter.com.

Need additional help reading documents?

More and more of our investors are using screen reading software as a quick and easy way to read their documentation if they are blind, partially sighted, or dyslexic. Alternatively, we can write to you in several alternative formats, such as large print, braille, audio, and OpenDyslexic font. Find out more about screen readers, accessing your documents online, and our alternative format options at quilter.com/document-help.

quilter.com This communication is issued by Quilter, a trading name of Quilter Investment Platform Limited. Quilter Investment Platform Limited is registered in England and Wales under number 01680071. Registered office at Senator House, 85 Queen Victoria Street, London, EC4V 4AB. Quilter Investment Platform Limited is authorised and regulated by the Financial Conduct Authority under reference number 165359. Quilter uses all reasonable skill and care in compiling the information in this communication and in ensuring its accuracy, but no assurances or warranties are given. Investors should not rely on the information in this communication when making investment decisions. Nothing in this communication constitutes advice or a personal recommendation. This communication is for information purposes only and is not an offer or solicitation to buy or sell any Quilter product. Data from third parties is included in this communication and those third parties do not accept any liability for errors and omissions. Investors should read the important information provided by the third parties, which can be found at quilter.com/third-party-data. Approver: Quilter March 2026 QI 26736/205/15107